Loading...

June 01, 2020 | Chart

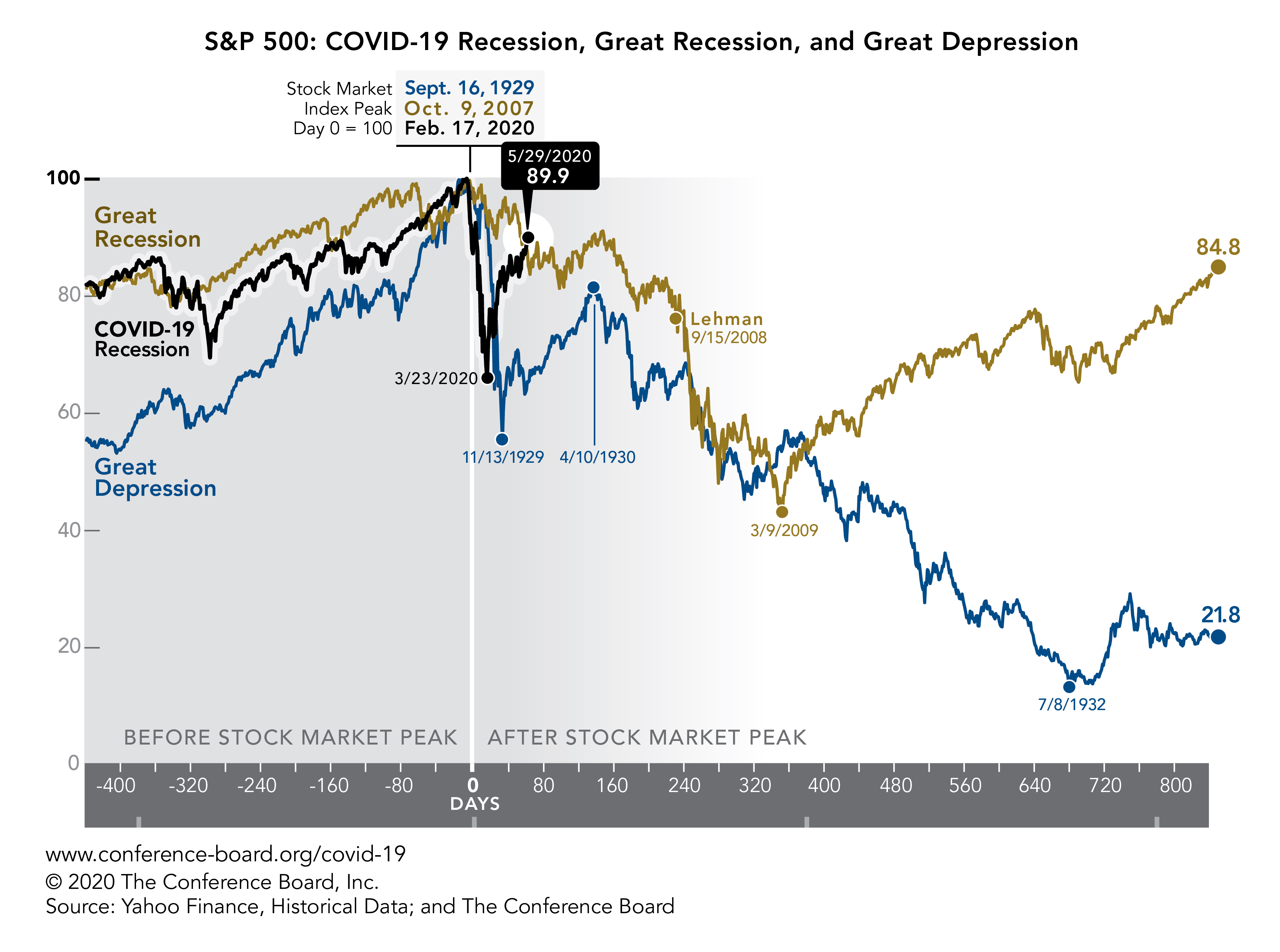

Does the recent V-shaped recovery of the S&P 500 suggest the worst of the COVID-19 crisis is over? Comparisons to past crises show this will not necessarily be the case.

As past crises have taught us, an initial stock market rally is no guarantee that we are out of the woods. The effectiveness of monetary and fiscal stimulus will only become clearer in the coming months. New stock market shocks, stemming from the pandemic or geopolitical tensions, could cause a return to volatility and new declines.

July 27, 2022 | Newsletters & Alerts

May 11, 2022 | Newsletters & Alerts