Loading...

11 June 2026 / Report

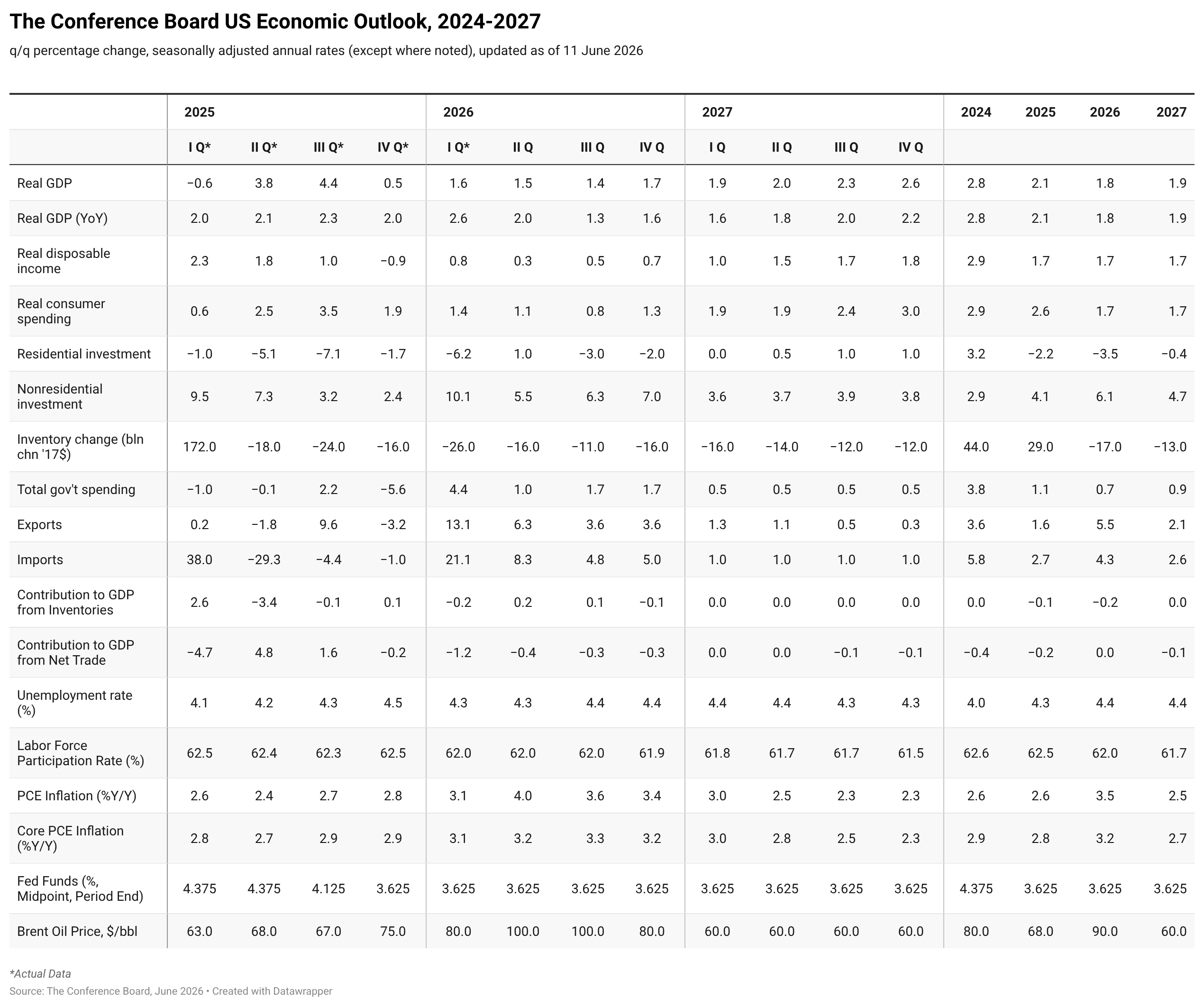

Consumer spending, the primary engine of U.S. economic growth since the pandemic, is showing increasing signs of fatigue as higher inflation and elevated energy costs erode household purchasing power. Recent declines in real disposable income, weaker inflation-adjusted retail sales, and subdued consumer confidence suggest that growth momentum is slowing even as labor market conditions remain resilient. The war in the Middle East has amplified these pressures through higher oil prices and broader supply-chain effects, reinforcing our expectation that economic growth will moderate in 2026. Before the start of the war, consumers were already under pressure as 2025 tariffs continued to pass through into retail prices and wage growth normalized from elevated post-pandemic rates. Real consumer spending has slowed materially, as recent data suggest that inflation-adjusted income growth is falling. An additional tax in the form of higher gasoline prices is likely to intensify these pressures. As fuel expenditures are difficult to reduce in the short run, households typically respond by cutting back on discretionary spending elsewhere.U.S. Outlook: Growth Shifts Gears from Consumers to Investment

Even if diplomacy regarding the conflict in the Middle East prevails, the negative economic ripple effects from the shock are already in motion. As a clear resolution to the conflict remains uncertain and likely to follow a non-linear path, a prolonged stalemate may be the most likely outcome. Against this backdrop, disruptions affecting the Strait of Hormuz will continue to weigh on global trade and economic activity while keeping energy markets vulnerable to renewed volatility.

The Conference Board therefore continues to forecast higher inflation and slower growth. Higher inflation will divert limited household resources toward energy and other affected goods and services, weighing on real consumer spending.

Consumers have been the primary driver of economic growth throughout the post-pandemic expansion. However, recent data suggest AI-related capital expenditures increasingly emerge as a key source of economic growth. Firms across a wide range of industries are ac

myTCB® Members get exclusive access to webcasts, publications, data and analysis, plus discounts to events.

Charts

The Gray Swans Tool helps C-suite executives better navigate today’s quickly developing economic, political, and technological environments.

LEARN MORECharts

Preliminary PMI indices show no change in weak DM growth momentum in November

LEARN MORE

Charts

How Might the World Fall Back into Recession?

LEARN MORECharts

Passing increases downstream, cutting costs, and absorbing price increases into profit margins are the chief ways to manage rising input costs. Few see changing

LEARN MORECharts

US continues to lead global productivity race

LEARN MORECharts

The Global Economic Fallout of the Ukraine Invasion

LEARN MORECharts

The global supply chain disruption associated with the COVID-19 pandemic has resulted in production delays, shortages, and a spike in inflation in world.

LEARN MORECharts

The Conference Board recently released its updated 2022 Global Economic Outlook.

LEARN MORE

Connect and be informed about this topic through webcasts, virtual events and conferences

PRESS RELEASE

LEI for South Korea Increased Sharply in May

July 08, 2026

PRESS RELEASE

US Consumer Confidence Inched Up in June

June 30, 2026

PRESS RELEASE

The Global LEI Inched Down in April, and Remained Unchanged in May

June 29, 2026

PRESS RELEASE

LEI for China Ticked Down in May

June 25, 2026

PRESS RELEASE

LEI for Mexico Declined in May

June 24, 2026

PRESS RELEASE

LEI for Australia Rose in April

June 19, 2026

All release times displayed are Eastern Time

This report identifies trends to help businesses prepare for an environment with more challenges for labor and capital but improvements in productivity growth.

LEARN MOREConnect and be informed about this topic through webcasts, virtual events and conferences

Volatility Notwithstanding, Labor Market Signals a Fed on Hold

July 02, 2026 | Brief

May Spending Rebounds, but Inflation Takes Its Toll

June 25, 2026 | Brief

The Conference Board Economic Forecast for the Euro Area Economy

June 19, 2026 | Report

FOMC Decision: There’s a Task Force for That

June 17, 2026 | Brief

June FOMC Preview: Meet the Warsh Fed: Rates on Hold, Communication in Focus

June 16, 2026 | Brief

June 12, 2026 | Report

USMCA 2.0—Trade Uncertainty in North America

June 10, 2026

Power Shifts: From the Fed to EV Markets

May 13, 2026

The Iran Conflict: Risks for the Global Economy

April 15, 2026

Priced Out: The State of US Housing Affordability

February 11, 2026

The CEO Outlook for 2026—Uncertainty, Risks, Growth & Strategy

January 15, 2026

The Big Picture: What's Ahead for the Global Economy?

December 10, 2025