Making Intangibles Tangible: Not Including Intangible Assets in Financial Statements Can Lead to Consequences

22 Oct. 2019 | Comments (0)

Despite their importance, internally grown intangible assets such as brands are not included in financial statements. This absence stems from the U.S. Generally Accepted Accounting Principles and results in a lack of accountability for managers and a lack of transparency for investors.

We need a new conceptual model that incorporates the idea that intangible assets directly connect to business strategy. That way, they can financially impact both revenue growth and shareholder value. After all, a company develops its brand to improve its bottom line because consumers prefer to purchase from companies they know and favor. The same holds true for investors who buy the stock of companies they know and trust.

To be clear, I am not recommending new accounting standards or arguing for existing ones to be changed in the immediate future. Rather, I seek to make the return on investments in intangible assets more transparent with supplemental financial reporting and to provide useful insights for the key stakeholders who require this information.

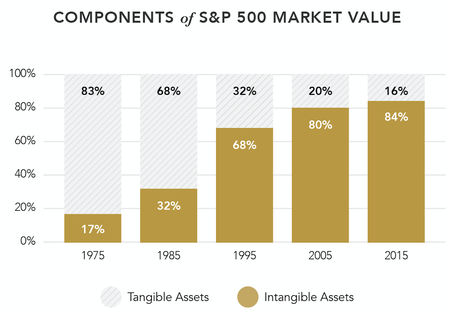

How much of a company’s value is derived from intangible assets?

While it is difficult to put a specific value on intangible assets, the growth performance of companies that invest in them is illustrative.According to the consulting firm Ocean Tomo, intangible assets grew as a portion of total enterprise value from an average of 17% of market cap in 1975 to 84% of the value of a company in the stock market in 2015 (see Figure 1).

Figure 1. Components of S&P 500 market value growth of intangible assets.*

*Adapted From “Intangible Asset Market Value Study, 2017,” by Ocean Tomo, LLC, 2017. Reprinted with permission. © Copyright by Ocean Tomo, LLC.

In 2018, Brand Finance published a Global Intangible FinanceTracker that examines the reported intangible assets as well as the estimated intangibles that go unreported for major corporations around the world. An extrapolation of the data finds that, on average, 92% of the total value of the top 10 companies (based on intangible asset value) is comprised of intangible assets. These companies only reported an average tangible net asset value of 14%, with net disclosed intangibles of 4% and disclosed goodwill of 6%, most likely resulting from mergers. This puts the undisclosed intangible assets of these companies at 75% (meaning three-quarters of their total corporate value is unaccounted, unreported, and unmanaged).

Admittedly, the top 10 companies (Amazon, Microsoft, Apple, Alphabet, Alibaba, Facebook, Tencent, Johnson & Johnson, AT&T, and Anheuser-Busch InBev) are tech-strong. But, even among the top 100 companies on the list, the average intangible value came in at 88% of the total enterprise value. In an ideal world, these huge intangible assets would be measured, valued, and managed like other business assets.

I helped pioneer a quantitative research study called the CoreBrand Index®. It’s a set of tools developed to help executives project potential future results of strategic changes made to their corporate brands, which ultimately impacts enterprise value. The extensive research, which has been fielded consistently over three decades, finds that corporate brands have two primary financial effects on a company: revenue premium and stock premium.

When it comes to revenue premium, consumers prefer to do business with companies they know and like, which impacts current and future revenues. Then there’s stock premium: Investors prefer to buy the shares of businesses they know and favor. Through regression analysis of the factors that drive stock performance, evidence indicates that cash flow, expected cash flow, earnings growth, dividends, as well as corporate brands all play a role in stock valuation. Thus, the corporate brand of a company performs a measurable function in providing a premium on the company’s stock price to varying degrees across all the companies and industries tracked.

While there is overwhelming evidence of intangible asset value when a company is sold and goodwill is placed on the balance sheet, this integral value is essentially unaccounted when the company is running at pace. Even when goodwill is on the balance sheet it is subject to annual impairment checks, but with no ability to value accretion. This need for a management tool that will provide better accountability is driving the development of a theory of intangible capital.

I agree with Brand Finance CEO David Haigh, who states in the Global Intangible Finance Tracker report:

We urgently need a more imaginative approach towards a regular revaluation and reporting of intangible assets. If we could achieve a more meaningful reporting approach we believe that it would lead to better informed management, higher investment in innovation and intangible asset value creation, stronger balance sheets, better defense against asset strippers, and generally serving the needs of all stakeholders.

Making intangibles tangible is a project to share ideas and methods of measuring, valuing, and managing intangible assets for value creation. Ocean Tomo has identified the size of intangible assets. Brand Finance examines both reported and unreported intangible assets. Tenet’s CoreBrand approach uses a market-based quantitative research tool as a way for businesses to manage intangible assets for value creation. If there are other systems being utilized by Conference Board members, I would be happy to report about them in future blogs.

See author James Gregory share insights on The Market is Watching: How Innovation Cultures Are Valued at Innovation: The Culture/Metrics Summit, December 10-11, 2019 in New York City.

This post is the third in a series on intangible assets. Check out past posts below:

-

About the Author:Dr. James Gregory

Dr. James R. Gregory is a leading expert on measuring the strength of intangible assets and the resulting impact on corporate financial performance. He is chairman emeritus of Tenet Partners, where he…

0 Comment Comment Policy