.png)

.png)

Loading...

August 15, 2022 | Article

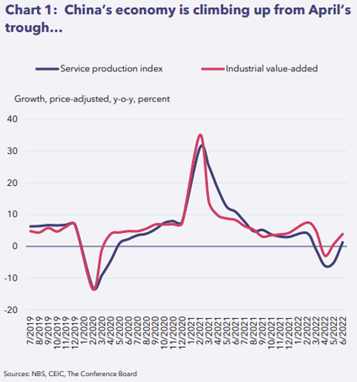

In our August Global Economic Outlook update, we downgraded GDP growth for China for the full year of 2022 by 0.3 percentage points. This is to account for a weaker-than-expected services recovery in the second half of the year, due in part to renewed surges in COVID-19 infections over July and August that are dampening consumption. Still, another monthlong full city lockdown, which occurred in Shanghai in the second quarter, is not in our base case. Our annual growth forecast for official Chinese GDP for 2022 is currently at 3.7 percent, while our 2023 forecast is unchanged at 5.3 percent.

Investment has diverged recently, with relatively robust manufacturing and infrastructure investment but contractions in the real estate sector. Despite our expectations for increased policy support from the Chinese government, we believe this trend will carry forward into the second half of 2022. Flagging confidence among prospective home buyers, a weak outlook for property prices, and liquidity constraints amongst developers will all drag down property investment growth.

While recent data suggest that China’s consumption slump may have bottomed, consumer confidence remains very weak. Lackluster domestic demand, COVID-19 restrictions, and the global economic slowdown will continue to weigh on Chinese consumption, both online and offline. For more analysis on consumption trends in China, please see our China Consumption Outlook (Q3 2022).

China’s export growth, measured in nominal value, stayed robust during H1, but volume growth has already moderated. High inflation, rising borrowing costs, and a looming global recession will inevitably curb consumer spending and business investment in advanced economies, which lead us to anticipate a more rapid deceleration in China’s export growth over H2.

For more analysis on economic trends in China, see our Economy Watch: China View (July 2022).