Fed hikes by 25 bps, but indicates terminal rate is close

01 Feb. 2023 | Comments (0)

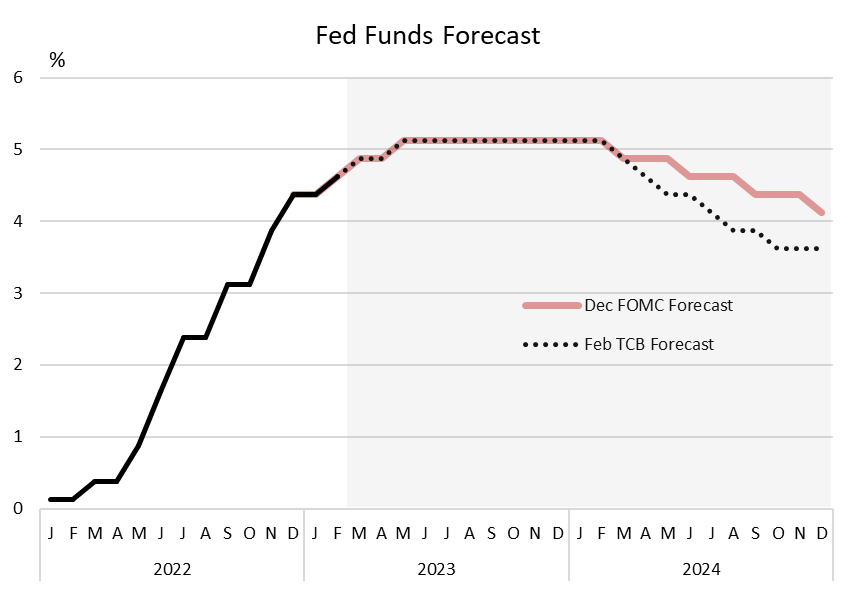

The Fed hiked interest rates by 25 basis points today, as expected. Chair Powell said that he expects “a couple” more small rate increases will be appropriate over the coming months and rate cuts are unlikely this year. We agree that rate cuts are unlikely in 2023, and are raising our Fed Funds forecast by 25 basis points to incorporate this new guidance.

Chair Powell said progress is being made on inflation, but that much work remains. He repeatedly said that inflation in core services ex-housing (or “super core” inflation) remained too high, but that the trend in goods inflation was positive and relief in housing inflation was “in the pipeline.” While Chair Powell expects the US economy to soften in 2023, he continues to expect the Fed to be able to achieve its 2 percent inflation target without a big downturn in jobs and the economy. When asked about the prospects for a US default, Chair Powell said that he expects the US Congress will raise the debt ceiling. He also said that no one should assume that the Fed can protect the economy if default occurs.

Businesses should expect interest rates to rise further over the coming months and to remain high through the end of the year. As the full impact of these rate hikes continues to weigh on the economy, The Conference Board forecasts that a recession will begin in early 2023 and run three quarters.

What were the Fed’s actions?

The Fed hiked by another 25 basis points in February and pushed the Fed Funds window to 4.50 – 4.75 percent. This was the Fed’s 8th consecutive hike, bringing the cumulative increase in interest rates to 4.5 percent this cycle. Rates are now deep in ‘restrictive’ territory (anything above 3 percent). The Fed also said that there will be no change to its ongoing plan to reduce the size of its balance sheet, which was first unveiled in May 2022. Today’s actions were unanimously approved by the members of the Federal Open Market Committee.

What does this mean for the US economy?

The Federal Reserve’s actions today were widely anticipated, but its tone about the future shifted somewhat. In the policy statement, the FOMC said “In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” In previous statements it had used the word pace, which suggests that the Fed is closing in on a terminal rate. However, as noted above, Chair Powell said that once a terminal rate is reached he does not expect the Fed to cut rates in 2023. Thus, interest rates should rise further over the coming months and are unlikely to fall this year.

Since tightening started in March 2022, the Fed Funds rate has risen by a total of 450 basis points. As a function of this, interest rates throughout the economy have risen rapidly. Tighter policy has begun to cool the overall economy—though with a lag. While the labor market remains exceptionally tight, other parts of the economy have begun to slow (like consumption and nonresidential investment) while other parts have begun to contract (like residential investment). As the full impact of this year’s Fed Funds hikes continues to weigh on businesses and consumers, economic activity will slow further—tipping the economy into a broad, but shallow, contraction. We forecast that a recession will begin in Q1 2023 and will last for three quarters.

-

About the Author:Erik Lundh

Erik Lundh is Senior Global Economist for The Conference Board Economy, Strategy & Finance Center, where he focuses on monitoring global economic developments and overseeing the organization&rsquo…

0 Comment Comment Policy