October inflation saw some relief, but remains high

10 Nov. 2022 | Comments (0)

The headline Consumer Price Index (CPI) eased somewhat in October along with Core CPI, which excludes food and energy. While these data show some progress in the Fed’s fight against inflation, we continue to expect additional interest rate hikes over the coming months and a recession to begin around the end of the year.

Insights for What’s Ahead

- These October CPI readings showed some welcome relief on inflation and are consistent with our forecast that topline year-over-year CPI growth probably peaked in Q2 2022. Still, the readings remain near four-decade highs. The improvement in the headline reading was fairly broad-based, with many components showing moderating month-over-month price increases or even contractions. However, this progress was offset by elevated shelter and energy prices.

- We expect the Fed to hike by 50 bp in December pushing the Fed Funds window to 4.25-4.50 by the end of the year, and then up to 4.75-5.00 percent in early 2023—deep into “restrictive” territory. Even with this degree of monetary policy tightening, key consumer price indexes, specifically the personal consumption expenditure deflator, will likely remain above the 2 percent target (we forecast 2.5 year-on-year) by the end of 2023. We do not expect the Fed to lower rates next year.

- Borrowing costs will remain elevated in the near-term as the Fed battles inflation. These two forces will weigh on consumer spending and business investment over the next 12 to 18 months and will likely trigger a US recession. Anemic growth and elevated inflation before and after this recession will exhibit stagflationary characteristics.

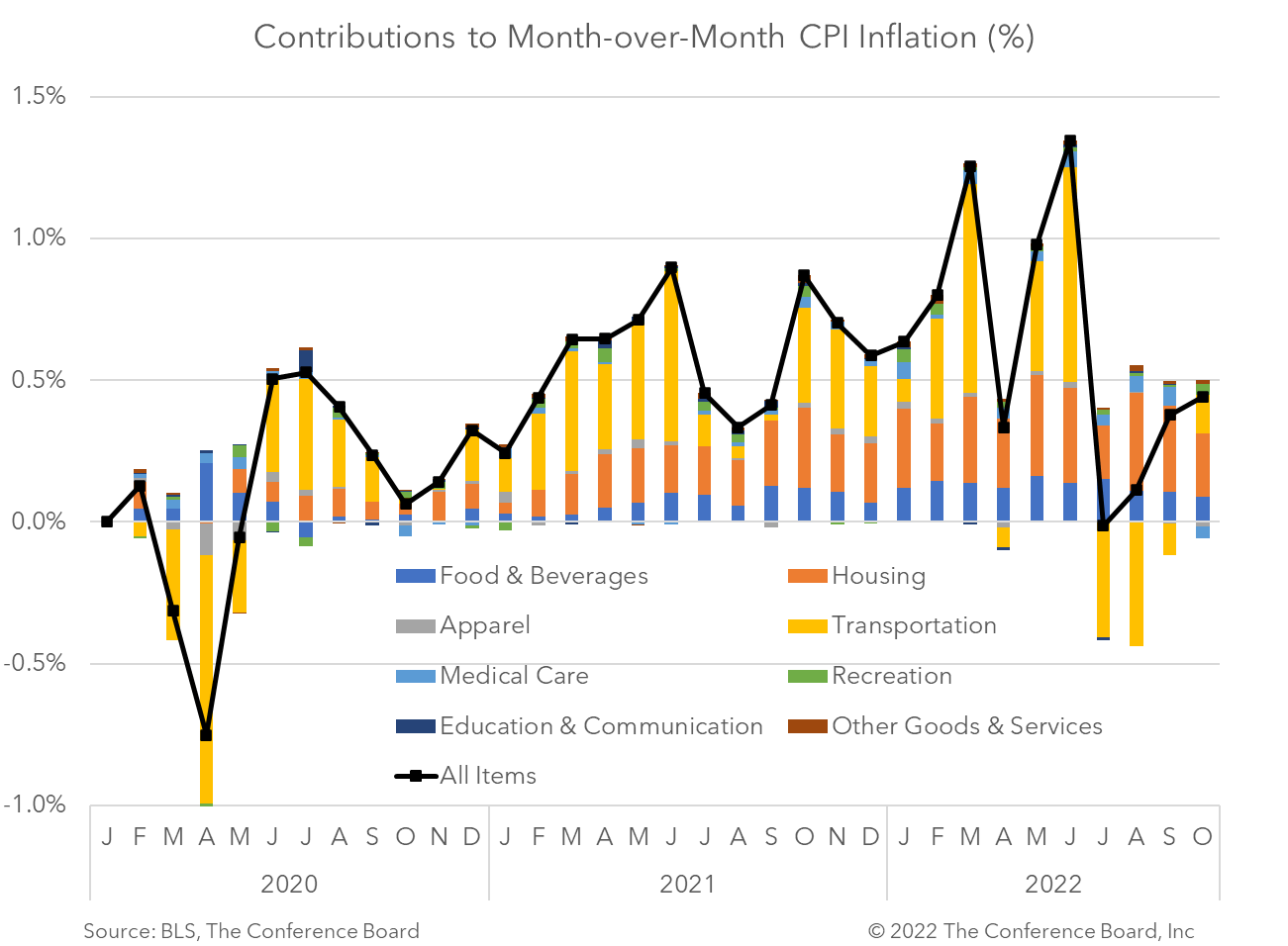

October Inflation Highlights

Headline CPI slowed to 7.7 percent year-over-year in October, vs. 8.2 percent in September. In month-over-month terms, however, this topline inflation metric was 0.4 percent—flat from the month prior. Many index components saw price gains moderate for the month, and some (including used vehicles and apparel) saw prices decline. However, shelter prices remained high and energy price gains accelerated.

Core CPI also moderated in October. The core index, which is total CPI less volatile food and energy prices, rose by 0.3 percent month-over-month in October, vs. 0.6 percent in September, and 0.6 percent in August. In year-over-year terms core CPI was rose to 6.3 percent from 6.6 percent in September.

-

About the Author:Erik Lundh

Erik Lundh is Senior Global Economist for The Conference Board Economy, Strategy & Finance Center, where he focuses on monitoring global economic developments and overseeing the organization&rsquo…

0 Comment Comment Policy