April CPI Moderates, but Inflation Remains Problematic

11 May. 2022 | Comments (0)

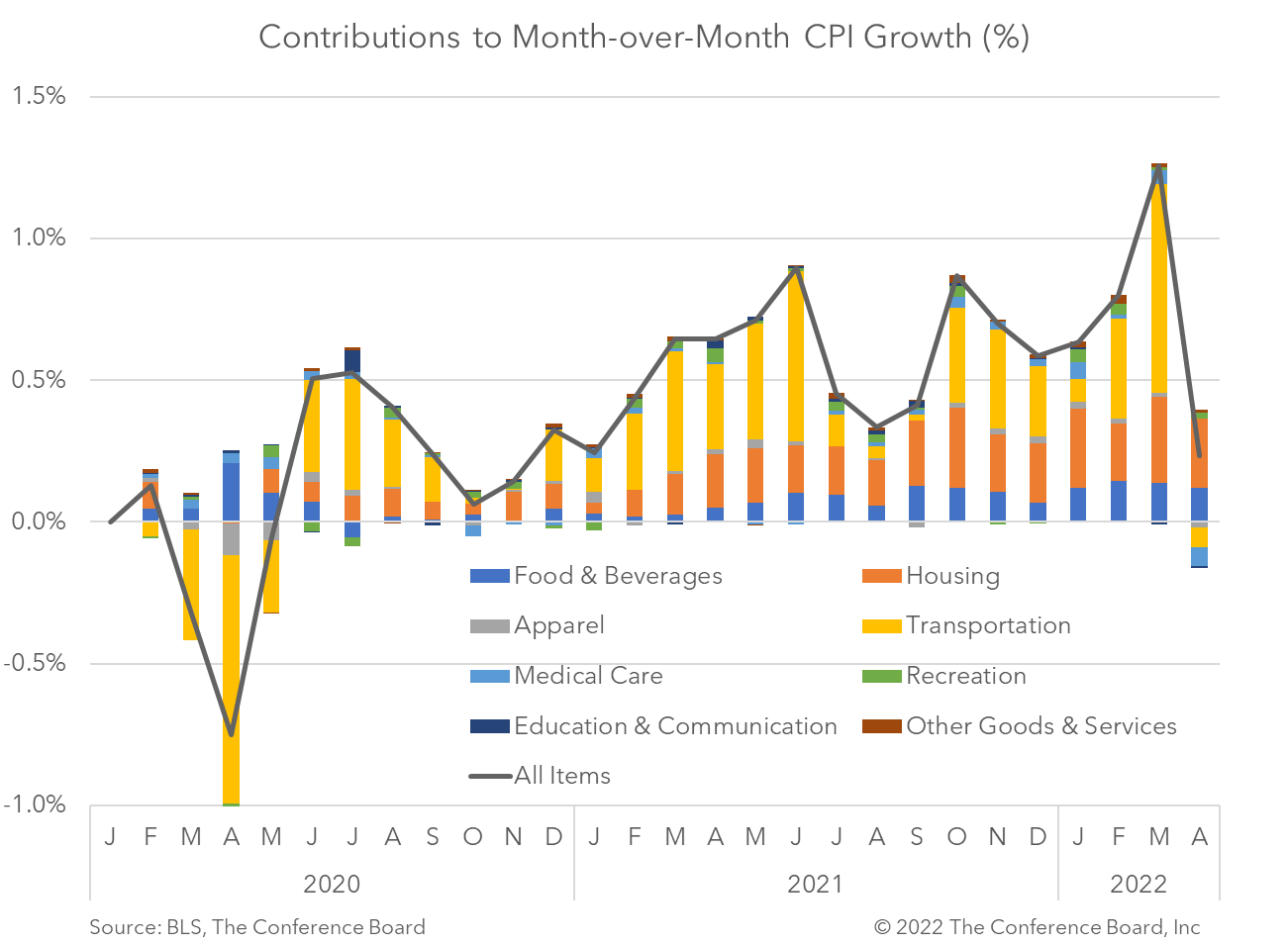

The Consumer Price Index (CPI) rose to 8.3 percent year-over-year in April, vs. an increase of 8.5 percent year-over-year in March. This is the first time this widely-followed gauge of inflation increased at a slower clip in eight months. Core CPI, which excludes volatile food and energy prices, slowed to 6.1 percent year-over-year, vs. 6.4 percent in March.

On a month-over-month basis, April CPI rose 0.3 percent, vs. 1.2 percent March. Meanwhile, April Core CPI rose 0.6 percent, vs. 0.3 percent in March. This direction divergence shows that energy prices cooled following a large spike in March, but that inflation in core parts of the economy may be intensifying. Indeed, while the index for gasoline fell 6.1 percent over the month, prices for shelter, airline fares, and new vehicles all rose. Meanwhile, food prices rose 0.9 percent from the previous month.

These price trends appear to be consistent with current events around in the world. Russia’s invasion of Ukraine sent oil prices soaring in late-February and March, but energy prices have retreated somewhat over the last month. Meanwhile, shocks to global agricultural prices associated with the conflict (Ukraine and Russia are major global grain producers) appear to be ongoing. Finally, COVID-19 outbreaks in China have resulted in lockdowns in numerous cities there, including Shanghai. The resulting disruption to production and export activity are once again cascading through global value chains. This still evolving story in China is important and may result in additional inflationary pressures in the coming months.

At present, our forecast for PCE inflation, which is similar to CPI, rises from a reported 6.3 percent year-over-year in Q1 2022 to a high of 6.6 percent in Q2 2022 and then slows to 4.2 percent in Q4 2022. We project that Core PCE inflation, which is similar to Core CPI, rises from a reported 5.2 percent year-over-year in Q1 2022 to a high of 5.9 percent in Q2 2022 and then slows to 4.4 percent in Q4 2022.

-

About the Author:Erik Lundh

Erik Lundh is Senior Global Economist for The Conference Board Economy, Strategy & Finance Center, where he focuses on monitoring global economic developments and overseeing the organization&rsquo…

0 Comment Comment Policy