Rising Inflation Slows Household Consumption

31 Mar. 2022 | Comments (0)

Insights for What’s Ahead

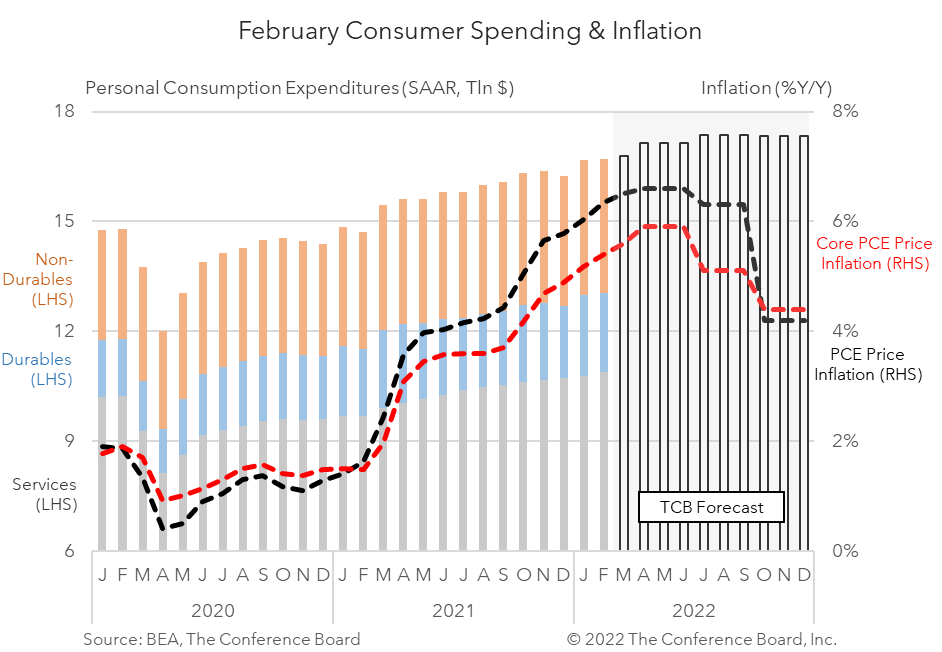

- Personal consumption slowed in February reflecting some likely payback from a surge in spending in January. Also, while spending on goods was tepid, outlays on services remained robust as the end of the omicron COVID-19 wave probably encouraged greater consumption of in-person services.

- However, spending in real terms declined as consumer price inflation continued to rise aggressively in the month. Year-over-year inflation for food at home reached new heights, and prices continued to swell for most other goods and services.

- The data do not reflect the war in Ukraine, as the invasion occurred late in the month. Still, we anticipate that continued supply chain disruptions from COVID-19 shutdowns abroad and spikes in commodity prices related to the war will continue to stoke inflation going forward, dampening consumption and thereby real GDP growth in 2022.

- We expect that PCE inflation, which the Fed watches, will remain well above 6 percent for much of the balance of this year and for real GDP growth to slow to 1.7 percent 4q/4q 2022 compared to 7.0 percent 4Q/4Q in 2021.

- Our estimates are among the more pessimistic of those surveyed by Blue Chip and Consensus Economics in March. Nonetheless, there are still downside risks to even our conservative projections.

Report Details: Somber News for Consumption

Consumer inflation continued to surge in February. Headline PCE price inflation increased by 6.4 percent year-over-year in February (the highest reading since 1982), vs. 6.0 percent in January. The BEA also reported that Core PCE Inflation, which excludes food and energy prices, rose to 5.4 percent year-over-year (the highest reading since 1983), vs. 5.2 percent in December. On a month-over-month basis, headline PCE price inflation was up at 0.6 percent in February, vs. 0.5 percent in January, while core PCE price inflation (total less food and energy) rose by 0.4 percent month-over month, following four months of 0.5 percentage point increases. The evolution of inflation in February is consistent with our anticipation that headline PCE inflation will remain well above 6 percent year-over-year for much of 2022, and that the core will linger above 5 percent for much of the balance of this year. Still, there are risks that our projections, which are amongst the highest relative to other forecasters in terms of the trajectory of inflation, could still be too low. The evolution of the war in Ukraine and COVID-19 lockdowns in China will play a key role in how high prices go.

Inflation is eroding households’ purchasing power. Overall personal income rose by 0.2 percent in February, following a modest 0.1 percentage point rise in January. Both employee compensation (+0.7 percent) and proprietors’ income growth (+0.8 percent) were healthy in the month. Government transfer payments declined a second month (-0.3 percent). Despite the increase in nominal personal income, real personal income, both overall and after taxes, continued to decline on rising inflation. Real total personal income fell by -0.1 percent month-over-month in February marking the sixth consecutive contraction, while real disposable personal income fell by 0.2 percent month-over month, tacking on a seventh month of decline.

Payback, the end of omicron, but also rising prices dampened consumption. Nominal personal consumption expenditures rose by just 0.2 percent month-over-month in February following a 2.7 percent jump in January. Again, some of the slowing in February likely reflected payback from January’s outsized increase, plus shifting demand away from durables (-2.5 percent) towards in-person services including healthcare (+0.6 percent), transportation (+3.0 percent), recreation (+2.7 percent), and hotels and restaurants (+3.0 percent) as omicron faded. However, after accounting for inflation, real personal consumption expenditures fell 0.4 percentage point in February, declining the third time in four months. Real goods spending was down 2.1 percent month-on-month. However, one bright spot is that real services increased by 0.6 percent in February, the fastest pace since July 2021 ahead of the delta COVID-19 variant.

-

About the Author:Erik Lundh

Erik Lundh is Senior Global Economist for The Conference Board Economy, Strategy & Finance Center, where he focuses on monitoring global economic developments and overseeing the organization&rsquo…

-

About the Author:Dana M. Peterson

Dana M. Peterson is the Chief Economist and Leader of the Economy, Strategy & Finance Center at The Conference Board. Prior to this, she served as a North America Economist and later as a Global …

0 Comment Comment Policy