Loading...

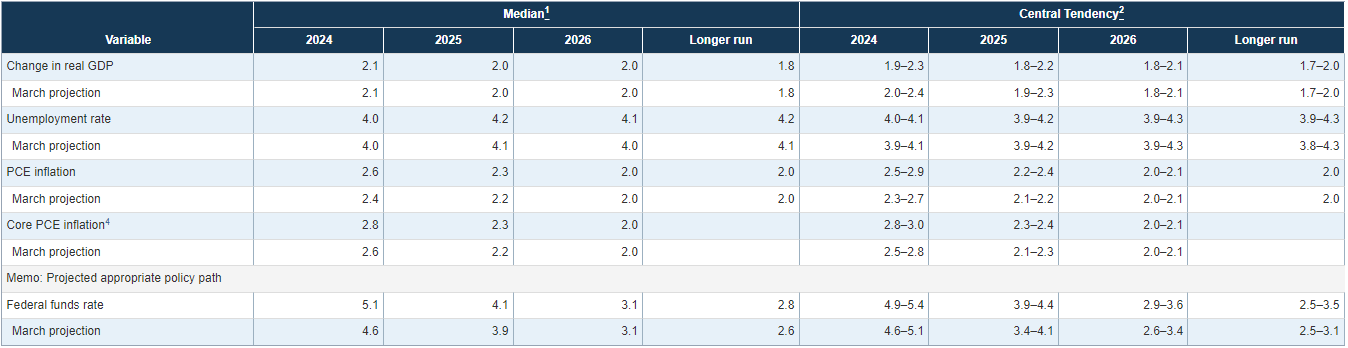

On the economy, Chair Powell said that the Fed expects GDP growth to slow from last year’s elevated pace as tight monetary policy and financial conditions continue to weigh on economic activity. This is unchanged from the March meeting. However, the June SEP showed that FOMC participants raised their expectations for inflation in 2024 and 2025. According to Chair Powell, this was due to the stalled progress on inflation seen in Q1 2024 and concerns about base effects in year-on-year inflation readings later this year. Also, the longer run outlook for inflation also rose as FOMC members increasingly believe that the neutral interest rate has drifted higher compared to prior to the pandemic. While inflation remains too high, Powell said that much progress toward achieving the 2% target was seen in 2023. He reiterated that the FOMC is waiting for more encouraging inflation data to come in before it starts to cut rates. He noted that today’s CPI report was unexpectedly encouraging, but that the Fed would need to see several months of similar data before cuts would occur. However, the June SEP does not anticipate lower inflation readings (like that seen today) to occur going forward. Our expectations for overall economic growth are more pessimistic for 2024, due to our forecast for a mid-year slowdown, but is similar to the FOMC’s for 2025. This weakness, in our view, should help lower inflation more rapidly than the June SEP suggests. Lower inflation should, in turn, yield two 25 bps interest rate cuts in Q4 2024. Finally, the June SEP saw an increase in the central tendency for longer run interest rates. This upward drift, according to Chair Powell, is due to an increased number of FOMC participants believing that the neutral rate has risen since the pandemic.

Highlights

At the June FOMC meeting, the Fed left rates unchanged and lowered its guidance on interest rate cuts to just a single 25 basis points reduction in 2024 (although many on the committee did think two cuts are still a possibility).What were the Fed’s actions?

After implementing 525 basis points of interest rate hikes since early 2022, the FOMC elected to hold the federal funds rate window at 5.25 – 5.50% again in June. Rates remain in ‘restrictive’ territory (anything above 3%). Regarding the Fed’s balance reduction program (known as Quantitative Tightening) there were no changes in June. The last set of changes occurred at the May FOMC meeting, where it announced that the pace of asset reductions would decelerate starting on June 1st.What are the Fed’s expectations for the future?

The Federal Reserve’s June SEP (see figure) painted a different picture of the future than the March SEP. Expectations on overall economic growth were unchanged, but FOMC committee members increased their inflation forecast for 2024 and 2025 and reduced their expectations on rate cuts to just a single 25 bps decrease this year (vs. three in the March SEP).

Members of The Conference Board get exclusive access to Trusted Insights for What’s Ahead® through publications, Conferences and events, webcasts, podcasts, data & analysis, and Member Communities.

Retail Sales Show Consumers Stock Up ahead of Tariffs

April 16, 2025

US Seeks Shipbuilding Revival, Muting of China Dominance

April 14, 2025

March CPI May Hint at Consumer Pullback as Tariffs Rise

April 10, 2025

The US-China Trade War Escalates

April 09, 2025

Reciprocal Tariffs Will Weaken US and Global Economies

April 03, 2025