Headline CPI eased in December while Core CPI rose

12 Jan. 2023 | Comments (0)

The headline Consumer Price Index (CPI) eased again in December while Core CPI, which excludes food and energy, rose somewhat. Lower energy prices were a large factor in lowering the headline December print. While this is mostly welcome news, much work remains to be done to bring inflation closer to 2 percent. We expect two more 25 bp interest rate hikes in February and March, and a recession to begin early this year.

Insights for What’s Ahead

- December CPI readings showed continued relief in inflation and are consistent with our forecast that topline year-over-year CPI peaked in Q2 2022. Still, the readings remain far too high. The improvement in the headline figure was largely driven by lower energy prices, although prices for many core goods also declined. However, core inflation ticked up slightly due to rising prices in core services, like shelter. As the housing market cools further over the coming months, shelter prices should gradually follow suit.

- We continue to expect the Fed to hike rates by 25 bp on February 1, pushing the Fed Funds window to 4.50-4.75. We expect one final 25 bp hike in March and then the Fed to keep rates elevated for the remainder of 2023. Even with this degree of monetary policy tightening, key consumer price indexes, specifically the personal consumption expenditure deflator, will likely remain above the 2 percent target until late 2024.

- Borrowing costs will remain elevated in the near-term as the Fed battles inflation. These two forces will weigh on consumer spending and business investment over the coming months and will likely trigger a US recession.

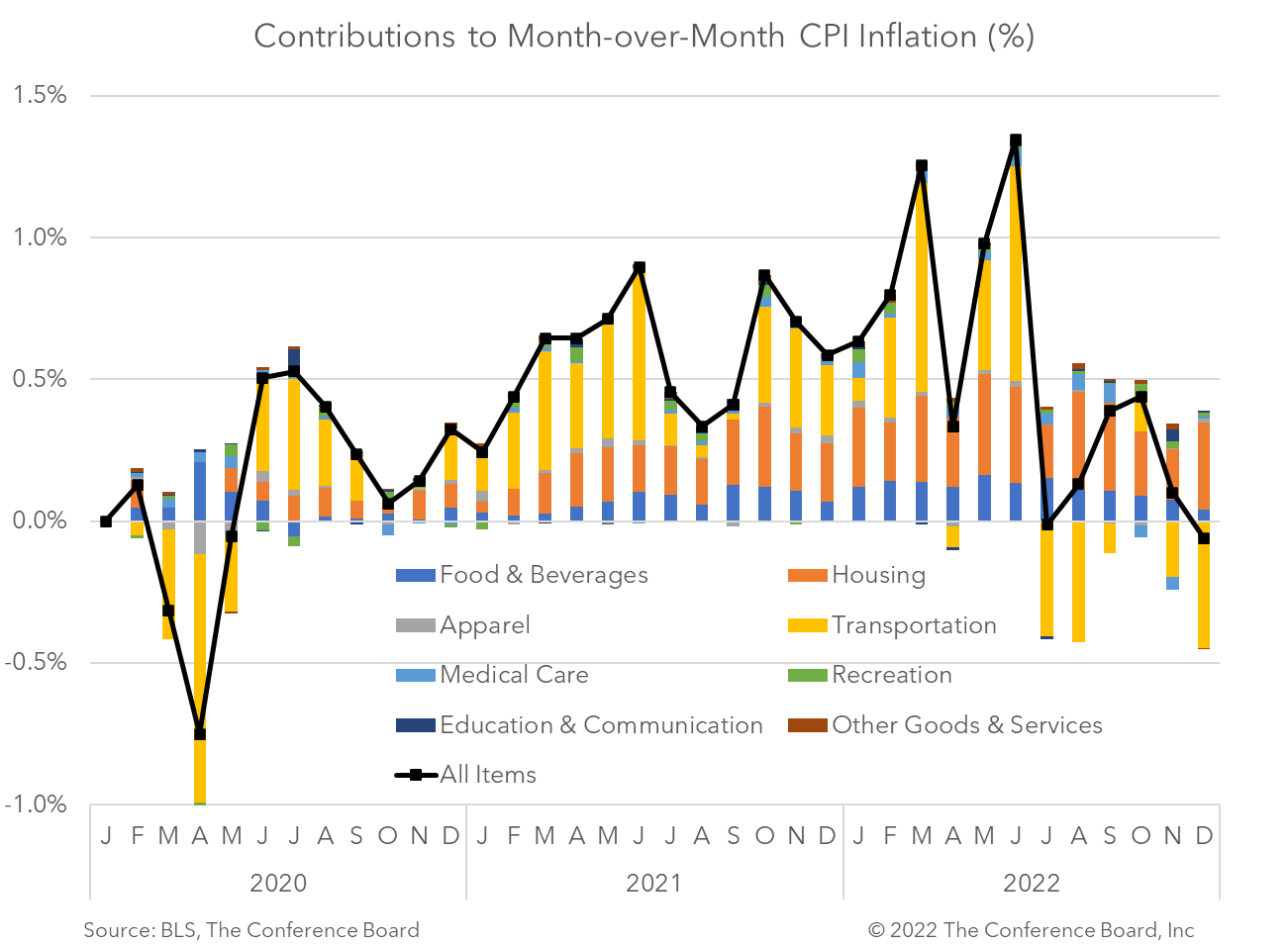

December Inflation Highlights

Headline CPI slowed to 6.5 percent year-over-year in December, vs. 7.1 percent in November. In month-over-month terms, this topline inflation metric fell to -0.1 percent, vs. 0.1 percent the month prior. This was the first month-over-month decline recorded since May 2020. Many index components saw price gains moderate for the month, and some (including energy, and both new and used vehicles) saw prices decline. However, shelter price gains remained high.

However, Core CPI rose somewhat in December. The core index, which is total CPI less volatile food and energy prices, rose by 0.3 percent month-over-month in December, vs. 0.2 in November, 0.3 in October, and 0.6 percent in September. Despite this uptick, year-over-year core CPI slowed to 5.7 percent from 6.0 percent in October due to base effects.

-

About the Author:Erik Lundh

Erik Lundh is Senior Global Economist for The Conference Board Economy, Strategy & Finance Center, where he focuses on monitoring global economic developments and overseeing the organization&rsquo…

0 Comment Comment Policy