Labor Market Remains Robust, But Deceleration Expected

05 Aug. 2022 | Comments (0)

Commentary on today’s U.S. Bureau of Labor Statistics Employment Situation Report

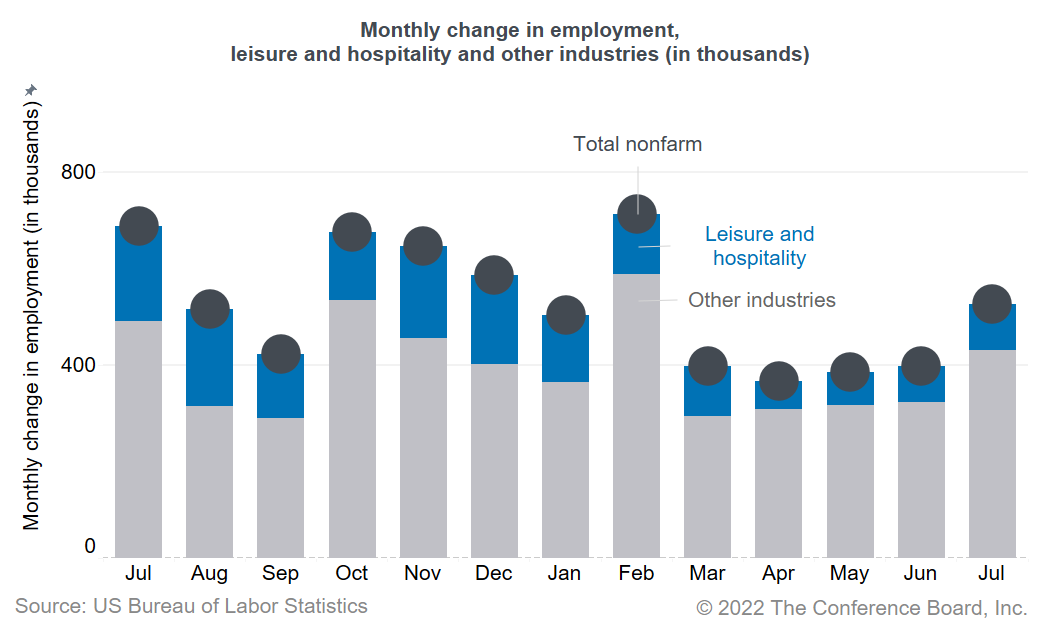

Today’s job report showed another strong month for payrolls, with 528,000 jobs added in July 2022, after an upwardly revised increase of 398,000 jobs in June. Thus far, the buoyant labor market is still defying headwinds in the rest of the economy, where economic activity has slowed. Usually, hiring decisions react to changes in business activity a few months later. Therefore, hiring is likely to decelerate over the coming months.

The unemployment rate ticked down to a historically low 3.5 percent in July 2022, down from 3.6 percent in June. The labor force participation rate decreased slightly to 62.1 percent in July, down from 62.2 percent in June. Overall, employment has now returned to its pre-pandemic level (February 2020). Job recovery has been somewhat slower for women, with employment still 0.1 percent below the pre-pandemic level, whereas employment for men now exceeds the pre-pandemic level by 0.2 percent.

Job growth remains strong in leisure and hospitality, which added 96,000 jobs in July, although recent job gains are twice as small as a year ago. Across most other industries job growth was strong. Jobs were gained in professional and business services (89,000), health care and social assistance (96,600), manufacturing (30,000), retail trade (21,600), and transportation and warehousing (20,900).

The labor market is still very tight and wage growth remains elevated. While job openings and quits rates are still historically high, job openings—a good leading indicator for employment changes—have fallen for three consecutive months. This may indicate that softening in labor demand lies ahead.

With inflation still elevated and the labor market robust, the Fed will likely continue to rapidly raise interest rates over the coming months. While economic output contracted for two consecutive quarters in the first half of 2022, a strong labor market means that currently we are likely not in recession. However, economic activity is expected to further cool towards the end of the year and it is increasingly likely that the US economy will fall into recession before yearend or in early 2023. The unemployment rate would likely rise following slowing economic activity and possible job losses although currently we expect the unemployment rate to remain below 4.5 percent in 2023. Labor force participation would decline as job opportunities diminish. Wage growth will likely cool as employee bargaining power weakens and businesses need to manage costs.

In reaction to slowing economic activity, companies will likely reduce or freeze hiring as a first step towards cost reductions. Depending on the gravity of the decline in economic activity, companies may reduce hours, bonuses, and wages, or turn to furloughs and layoffs. Lower-skilled workers would be more vulnerable to job losses, as also seen in earlier recessions when unemployment rates rose more for these workers. However, severe difficulties in finding and retaining workers over the last two years may prompt employers to be more careful about laying off workers. In addition, in in-person services, where the number of jobs is still recovering and 7 percent below pre-pandemic level, there may be less need for downsizing.

-

About the Author:Frank Steemers

The following is a bio or a former employee/consultant Frank Steemers is a Senior Economist at The Conference Board where he analyzes labor markets in the US and other mature economies. Based in New …

0 Comment Comment Policy