Loading...

February 11, 2021 | Chart

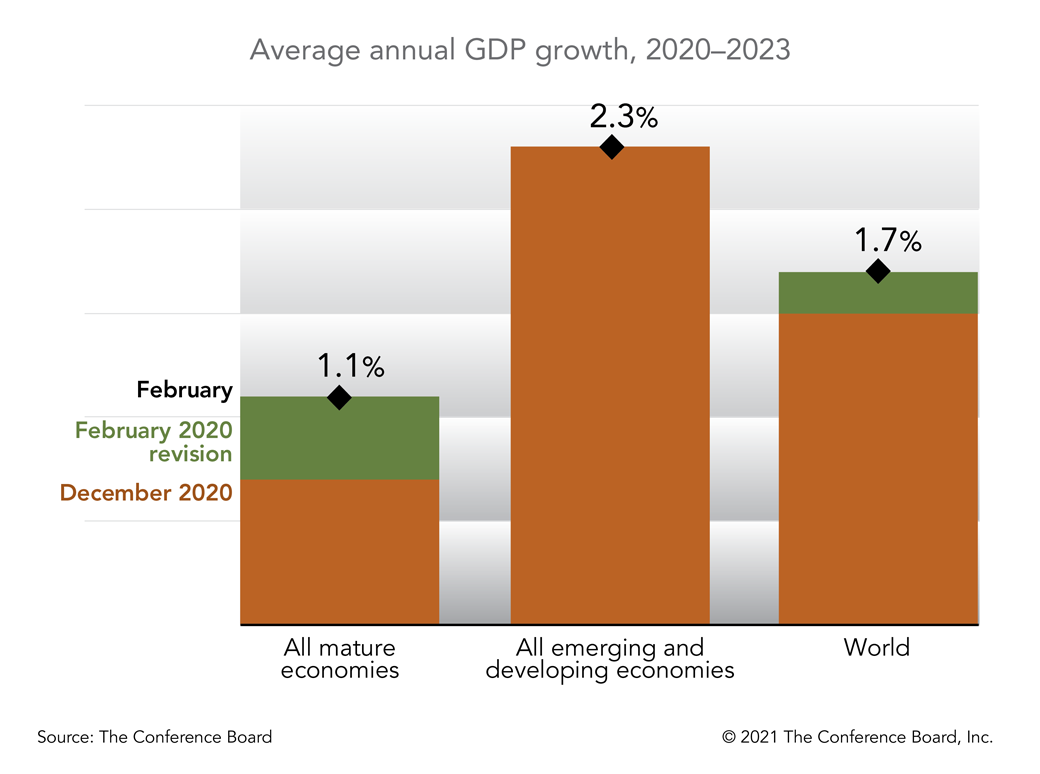

Our previous forecast for the global economy from 2020 to 2023 improved from 1.5 average annual GDP growth to 1.7 percent. The higher global growth rate is almost entirely driven by mature economies. Upward revisions to the 2020 growth rates in the US and Japan reflect the impact of additional fiscal support. Some of the improvement also represents “catch-up” growth in 2021 and 2022 that is above long-term potential. From 2023 onward, growth may return to more normal (and lower) rates, at 1.8 for the US and 0.9 for Japan. Upgrades to the outlook of other mature economies—including Israel, Taiwan, South Korea, and Australia—are related to relatively successful mitigation of the pandemic (or in the case of Israel, a successful vaccination campaign) and/or solid external demand for products related to technology and health care. Our average for the Euro Area from 2020 to 2023 remains essentially unchanged. Continued lockdowns, less robust fiscal stimulus packages compared to the US, and slower vaccination campaigns are contributing to a relatively subdued rebound in 2021 at 3.8 percent, following a contraction of 6.9 percent in 2020. However, we expect above potential growth in the Euro Area in 2022 (to 3.4 percent) and 2023 (to 1.9 percent), after which it eventually returns to our estimated long-term trend of 1.0 percent.

For more information: see GEO webpage