Job Growth Weakens as Renewed COVID-19 Uncertainty Looms

03 Dec. 2021 | Comments (0)

Commentary on today’s U.S. Bureau of Labor Statistics Employment Situation Report

Today’s jobs report showed weaker job growth in November compared to October. The labor market remains tight and still seems to be impacted by elevated Delta cases. While more people joined the labor force in November, the labor force participation rate remains well below its prepandemic rate. Overall,the labor market outlook is uncertain, as there are mounting downside risks linked to the newly identified Omicron variant of COVID-19.

Nonfarm payroll employment increased by 210,000 in November, after an upwardly revised increase of 546,000 in October. However, the unemployment rate decreased from 4.6 to 4.2 percent, and the labor force participation rate increased from 61.6 to 61.8 percent in November. This month, the results of the Establishment Survey (used for nonfarm payroll employment) and Household Survey (used for the unemployment rate and participation) were different, which makes interpretation of the results more difficult.

Job growth was weak in leisure and hospitality, adding only 23,000 jobs in November. Job growth in this area has slowed since the summer, averaging 93,000 between August and November, compared to 363,000 between April and July. Elevated Delta variant cases may still be hampering consumer spending on in-person services and therefore require less need for hiring. At the same time, labor shortages—which are especially severe for blue-collar and manual services workers—are making it harder for employers to recruit workers.

Job losses were also recorded in retail trade and motor vehicles and parts, which could be related to supply chain issues. On the other hand, transportation and warehousing,as well as professional and business services, added new jobs.

Recruitment and retention difficulties remain high. Average hourly earnings increased 4.8 percent over the past 12 months, and other labor market indicators also show severe hiring difficulties. For example, The Conference Board labor market differential—which is the percentage of respondents who say jobs “are plentiful” compared to the percentage of respondents who say jobs “are hard to get”—climbed further in November to the highest level in its 54-year history. Rising wages and labor shortages will feed into price inflation.

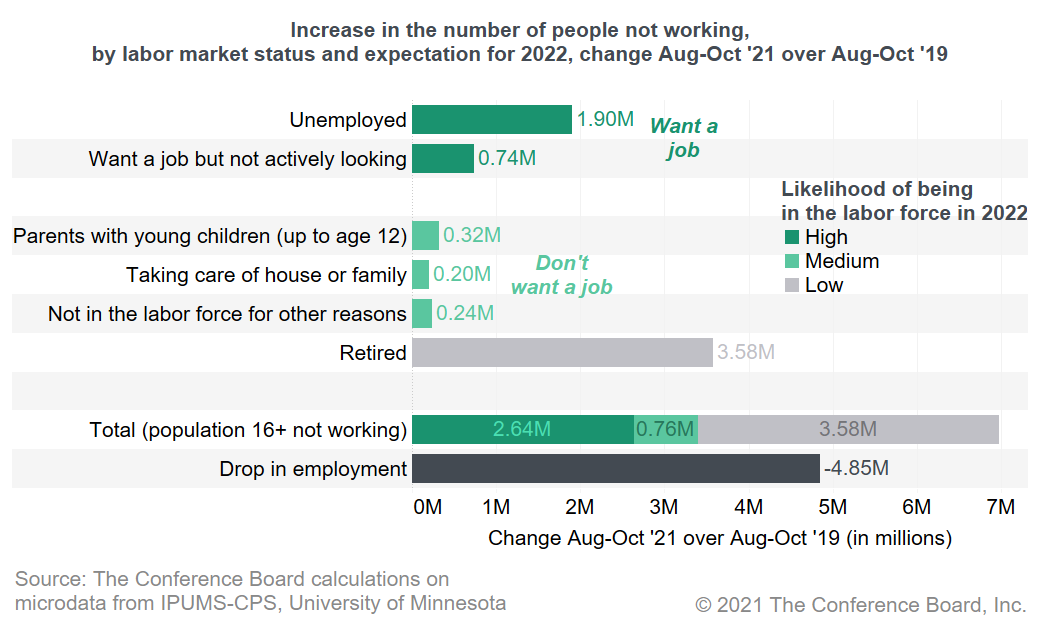

It is more likely now that hiring difficulties will continue into 2022. Labor force participation is still well below its prepandemic rate (61.8 percent in November 2021 compared to 63.3 percent in February 2020), and the likelihood of a full recovery in 2022 is low. In the chart we show the increase in the number of people not working in August-October 2021 relative to August-October 2019, for several groups. In total, the number of people aged 16 and above who are not working increased by 7 million during that time. 2.6 million of those are unemployed and people who want a job but are not actively looking. While the chance they will actively search or find a job in 2022 is high, they are a minority. About 4.3 million of them are people who currently do not want a job. Parents with young children, people doing household work or taking care of family, or others who currently do not want a job may return to the labor force if pandemic related constraints ease and job prospects further improve. On the other hand, most labor force exits were older workers who retired early (about 3.6 million), and the likelihood that many will return in 2022 is low.

Employers and policymakers will likely need to find other ways to deal with labor shortages or ensure continued job growth, such as improving older worker retention rates, automating tasks, or increasing immigration.

-

About the Author:Frank Steemers

The following is a bio or a former employee/consultant Frank Steemers is a Senior Economist at The Conference Board where he analyzes labor markets in the US and other mature economies. Based in New …

0 Comment Comment Policy