Loading...

Timely insights from the Economy, Strategy & Finance Center

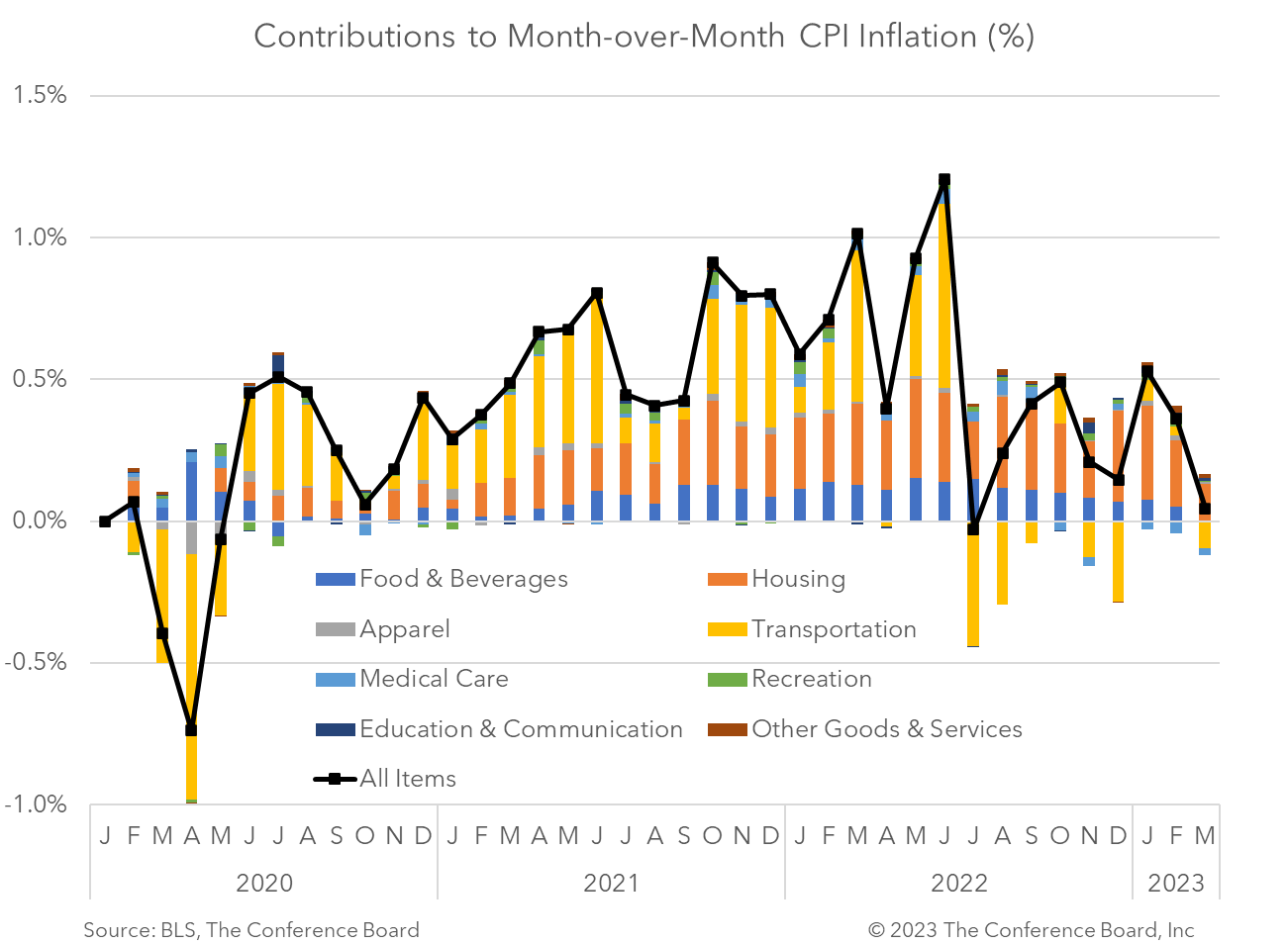

The March Consumer Price Index (CPI) showed that headline inflation slowed to 0.1 percent month-over-month (vs. 0.4% in Feb) and core inflation, which excludes food and energy, slowed to 0.4 percent month-over-month (vs. 0.5% in Feb). Year-over-year inflation rates for both the headline and core indices fell, but much more so for the headline index due to strong base effects. Many CPI components improved in the month, but rising shelter prices remained a major factor in the month-over-month increases in this month’s CPI readings. We do not believe these data are enough to keep the Fed from hiking rates further. March CPI readings showed relief across a variety of goods and services. For instance, food prices were flat for the month and energy prices fell. However, continued increases in shelter prices were responsible for approximately 60% of the inflation reported in the Core CPI. While relief in this key component of inflation is on the way, according to Chair Powell and private sector data on new rents, it will take time for the CPI numbers to fully incorporate this trend. While the 1.0 percent decline in topline year-over-year CPI looks like a big, positive development (and it is nice to see), it does not portend an end to the inflation debacle. This dramatic fall was due to base effects associated with the initial invasion of Ukraine one year ago, not a sudden turnaround in prices. Indeed, year-over-year Core CPI rose a touch for the month. We do not believe this CPI print puts the Federal Reserve in a position where additional rate hikes are no longer needed. We continue to expect two more 25 basis point hikes over the coming months and do not forecast any rate cuts until early 2024. Headline CPI slowed to 5.0 percent year-over-year in March, vs. 6.0 percent in February. In month-over-month terms this topline inflation metric fell to 0.1 percent, vs. 0.4 percent the month prior. According to the BLS, the index for shelter was the largest contributor to topline CPI this month. The energy index fell for the month and the food index was flat. Core CPI, which is total CPI less volatile food and energy prices, rose to 5.6 percent year-over-year in March, vs. 5.5 percent in February. The core index fell to 0.4 percent month-over-month in March, vs. 0.5 in February. As was the case with topline CPI, the increases in the core CPI was driven by shelter prices. Insights for What’s Ahead

March Inflation Highlights

Retail Sales Show Consumers Stock Up ahead of Tariffs

April 16, 2025

US Seeks Shipbuilding Revival, Muting of China Dominance

April 14, 2025

March CPI May Hint at Consumer Pullback as Tariffs Rise

April 10, 2025

The US-China Trade War Escalates

April 09, 2025

Reciprocal Tariffs Will Weaken US and Global Economies

April 03, 2025

Charts

Preliminary PMI indices show no change in weak DM growth momentum in November

LEARN MORECharts

Members of The Conference Board can access all underlying data of the Job Loss Risk Index by Industry in this Excel workbook.

LEARN MORECharts

While a US recession appears to be imminent, it will not look like any other in recent history.

LEARN MORECharts

CEOs’ views of current and future economic conditions remain pessimistic as they prepare for near-inevitable US and EU recessions.

LEARN MORECharts

The US economy appears to be on the precipice of recession.

LEARN MORECharts

Measure of CEO Confidence declined for the fifth consecutive quarter in Q3 2022 and has hit lows not seen since the start of the COVID-19 pandemic in 2020.

LEARN MOREPRESS RELEASE

US Leading Economic Index® (LEI) Fell in March

April 18, 2024

PRESS RELEASE

US Consumer Confidence Little Changed in March

March 26, 2024

PRESS RELEASE

US Leading Economic Index® (LEI) Inched Up in February

March 21, 2024

PRESS RELEASE

US Consumer Confidence Retreated in February

February 27, 2024

PRESS RELEASE

US Leading Economic Index® (LEI) Fell Further in January

February 20, 2024

PRESS RELEASE

CEO Confidence Improved in Q1 2024

February 08, 2024