Loading...

Timely insights from the Economy, Strategy & Finance Center

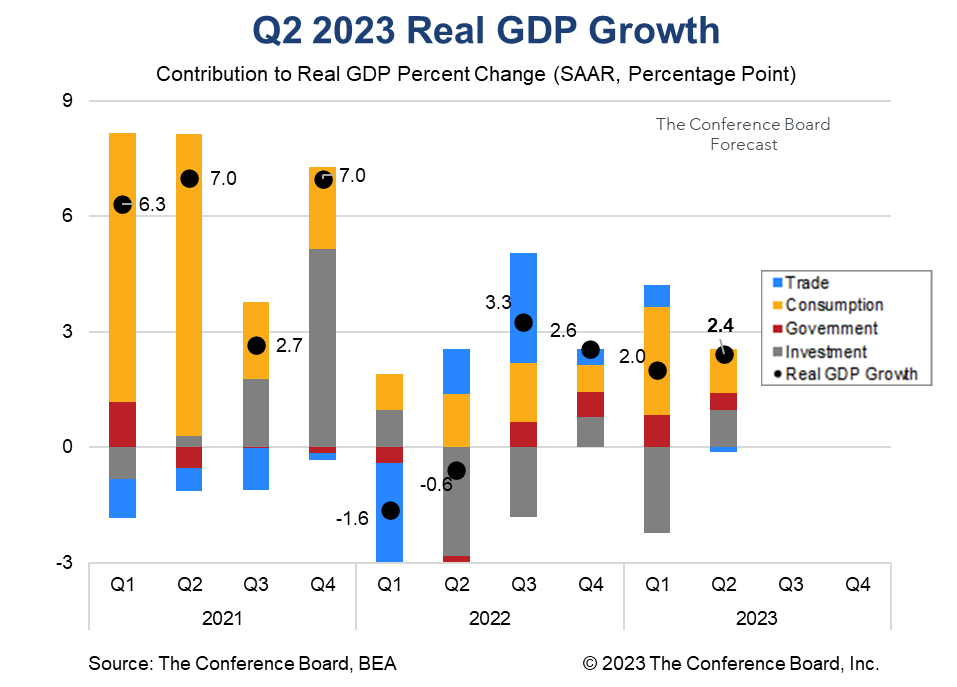

US Real Gross Domestic Product rose by 2.4 percent (annualized) during the second quarter of 2023, well above the consensus forecast of 1.8 percent* and The Conference Board’s forecast. Consumption growth cooled for the quarter, but improvements in business investment growth more than offset this. The prospects for a soft-landing for the US economy are rising, but The Conference Board projects that a short and shallow recession beginning later this year is more likely. GDP data in Q2 2023 showed a number of important trends that we expect to continue to play out over the year. Following a spike in consumption in Q1, due to high demand for durable goods, consumption in Q2 came in more muted. Growth in consumer spending on goods and (importantly) services both cooled for the quarter. As real disposable personal income growth cools, pandemic excess savings are depleted, and mandatory student loan repayment resumes, we expect consumption growth to weaken further and eventually dip into contractionary territory. The GDP data also showed a stronger than expected increase in non-residential investment in Q2. A spike in business investment in equipment (transportation equipment in particular) was a major driver of the strength. However, investment growth in structures and intellectual property products were also positive. Looking ahead, we expect weaker consumer demand and persistently high interest rates to reverse this trend. These and other recent data show that the US economy has been remarkably resilient to the duel stresses of high inflation and high interest rates. As inflation continues to cool it is possible that a soft landing may be achievable, but we continue to believe that a short and shallow recession is the more probable outcome. Considering today’s report, we are pushing our recession forecast out one quarter to Q4 2023. Personal Consumption Expenditures (PCE) expanded by 1.6 percent for the quarter, vs. 4.2 percent in Q1. Demand for goods grew by 0.7 percent (vs. 6.0 percent in Q1), while demand for services grew by 2.1 percent (vs. 3.2 percent in Q1). Additionally, as we already have monthly spending data for April and May, these quarterly data imply that consumer spending deteriorated in June. We’ll learn more about this in tomorrow’s Personal Income & Outlays report. On the investment side, nonresidential fixed investment grew by 7.7 percent, vs. 0.6 percent in Q1, due largely to strong investment in equipment for the quarter (10.8 percent). Residential investment grew by -4.2 percent, vs. -4.0 percent in Q1. This was the nineth consecutive quarter of contraction, but recent housing data suggests that growth may stabilize soon. Private inventories expanded by $9.3 billion**. This increase from $3.5 billion in Q1 resulted in a boost to US GDP growth of 0.1 percentage points. Government spending was a positive contributor to overall economic growth for the quarter, rising 2.6 percent, vs. 5.0 percent in Q1. The slowdown was largely associated with a decline in federal non-defense spending. Net exports contributed -0.1 percentage points to overall GDP. Exports grew by -10.8 percent for the quarter while imports grew by -7.8 percent. Finally, it is important to note that GDP data have undergone large revisions in recent quarters. For example, the advance estimate for Q1 2023 data was 1.1 percent, but was gradually revised up nearly a full percentage point to 2.0 percent. It is very likely that the final data for Q2 2023 will be quite different from these advance estimates. * Consensus data from Bloomberg

Key takeaways from today’s report.

The individual components of GDP were mixed.

Retail Sales Show Consumers Stock Up ahead of Tariffs

April 16, 2025

US Seeks Shipbuilding Revival, Muting of China Dominance

April 14, 2025

March CPI May Hint at Consumer Pullback as Tariffs Rise

April 10, 2025

The US-China Trade War Escalates

April 09, 2025

Reciprocal Tariffs Will Weaken US and Global Economies

April 03, 2025

Charts

Preliminary PMI indices show no change in weak DM growth momentum in November

LEARN MORECharts

Members of The Conference Board can access all underlying data of the Job Loss Risk Index by Industry in this Excel workbook.

LEARN MORECharts

While a US recession appears to be imminent, it will not look like any other in recent history.

LEARN MORECharts

CEOs’ views of current and future economic conditions remain pessimistic as they prepare for near-inevitable US and EU recessions.

LEARN MORECharts

The US economy appears to be on the precipice of recession.

LEARN MORECharts

Measure of CEO Confidence declined for the fifth consecutive quarter in Q3 2022 and has hit lows not seen since the start of the COVID-19 pandemic in 2020.

LEARN MOREPRESS RELEASE

US Leading Economic Index® (LEI) Fell in March

April 18, 2024

PRESS RELEASE

US Consumer Confidence Little Changed in March

March 26, 2024

PRESS RELEASE

US Leading Economic Index® (LEI) Inched Up in February

March 21, 2024

PRESS RELEASE

US Consumer Confidence Retreated in February

February 27, 2024

PRESS RELEASE

US Leading Economic Index® (LEI) Fell Further in January

February 20, 2024

PRESS RELEASE

CEO Confidence Improved in Q1 2024

February 08, 2024