Loading...

Timely insights from the Economy, Strategy & Finance Center

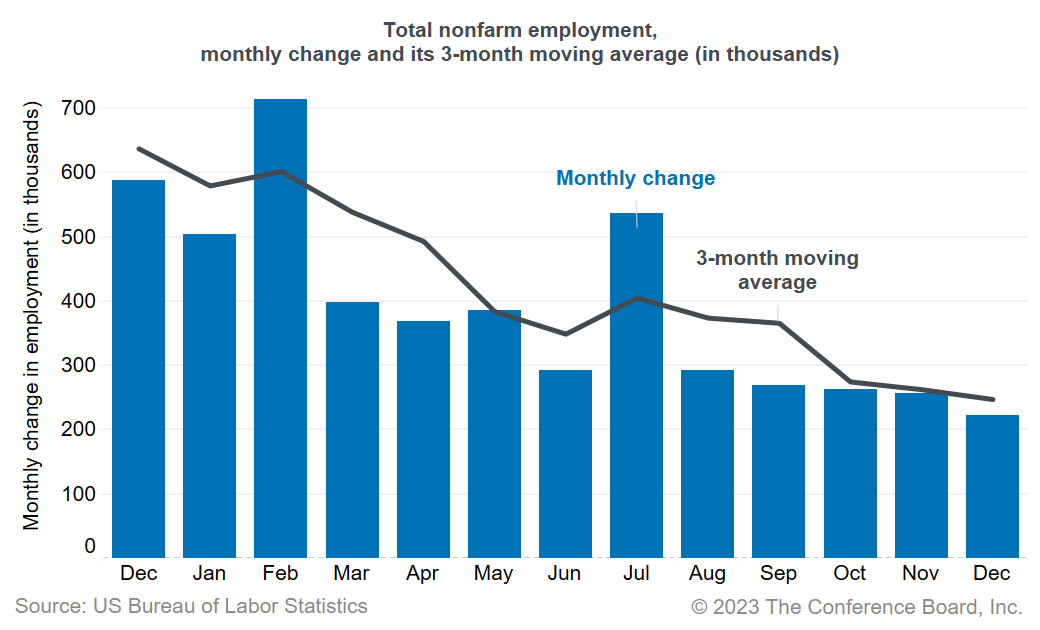

Today’s jobs report showed the US labor market is still strong, with 223,000 jobs added in December 2022, after an increase of 256,000 jobs (a downward revision) in November. Labor shortages persist due to structural factors—including, but not limited to, early retirements and reduced immigration. Demand for workers remains robust in in-person services such as health and social assistance and leisure and hospitality, putting continued pressure on wages as workers quit their jobs for better opportunities. Likewise, layoff rates are still below pre-pandemic levels. Year-over-year growth in average hourly earnings slowed to 4.6 percent in December—down from 4.8 percent in November, and its 2022 peak of 5.6 percent, reached last March. Even though job growth is still strong, we do expect slowing over the coming months in the labor market. December showed some signs of slowing labor demand: Jobs in temporary help services—a leading indicator for hiring—have now declined for five consecutive months. We are forecasting a recession to start in early 2023 as the Fed continues to raise its target interest rates to bring inflation under control, which will negatively impact labor demand. The unemployment rate fell slightly to 3.5 percent in December, down from 3.6 percent in November (a downward revision). By the end of 2023, we expect the unemployment rate to rise to 4.5 percent with the US economy slowing. The labor force participation rate for people aged 16 and older ticked up to 62.3 percent in December from 62.2 percent in November (an upward revision)—still a full percentage point below pre-pandemic levels. We expect labor force participation to decline further to 61.8 percent by the end of 2023. In December, notable job gains were reported in health care and social assistance (+74,400), leisure and hospitality (+67,000), and construction (+28,000). As consumers continue to shift their demand from physical goods to services, job gains in manufacturing continued its slow growth (+8,000), with job losses in non-durable goods (−16,000) partially offset by gains in durable goods (+24,000). There were slight job gains—when seasonally adjusted—in transportation and warehousing (+4,700), following job losses for four consecutive months. Retail employment increased after several months of declines, but is still on a slower trajectory, also consistent with slower demand for goods among consumers. Job growth in 2022—especially the first half of the year—was strong, with 4.5 million jobs added over the year. This was down from 6.7 million in 2021, but still much stronger than the 2 million jobs gained during 2019. Over 2022 as a whole, leisure and hospitality added 946,000 jobs, health care and social assistance added another 793,000, and professional and business services added another 605,000 jobs. Labor shortages are still a big challenge for employers. Approximately 2 million people retired earlier than anticipated in the last three years. The labor force participation rate among older workers (55+) declined to 38.8 percent in December—1.5 percentage points below the pre-pandemic rate. There is no immediate replacement for these workers. Moreover, an aging population means demand for services in health and social assistance will continue to stay strong. There were 1.9 million job openings in the industry—close to one million above pre-pandemic levels. There are few signs that suggest labor markets are significantly cooling. The quits rate (3 percent) is below its historic high (3.4 percent) observed at the end of 2021 but remains very high. The layoffs rate (1 percent) did not show any increase. We see some evidence of the Fed’s efforts impacting the labor market and cooling off labor demand for certain industries where spending is nondiscretionary. Temporary help services jobs have now declined for five consecutive months, quits rate in the information sector (which includes most tech companies) and construction are back to their pre-pandemic levels. These changes may bring some temporary easing of labor shortages in 2023 in these industries. However, once the Fed starts easing monetary policy—likely in 2024 after bringing inflation under control—labor demand may quickly recover, and worker shortages could reappear as the main challenge for employers. Commentary on today’s U.S. Bureau of Labor Statistics Employment Situation Report

Report Details

March Payrolls: The Calm Before the Tariff Storm

April 04, 2025

February Jobs Report Hints at Growing Uncertainty

March 07, 2025

Stability Underneath January’s Noisy Jobs Report

February 07, 2025

Q4 ECI Wage Deceleration Slows

February 07, 2025

Robust Job Gains Close 2024

January 10, 2025

November Job Gains Rebound from Disruptions

December 06, 2024

Charts

Preliminary PMI indices show no change in weak DM growth momentum in November

LEARN MORECharts

Members of The Conference Board can access all underlying data of the Job Loss Risk Index by Industry in this Excel workbook.

LEARN MORECharts

While a US recession appears to be imminent, it will not look like any other in recent history.

LEARN MORECharts

CEOs’ views of current and future economic conditions remain pessimistic as they prepare for near-inevitable US and EU recessions.

LEARN MORECharts

The US economy appears to be on the precipice of recession.

LEARN MORECharts

Measure of CEO Confidence declined for the fifth consecutive quarter in Q3 2022 and has hit lows not seen since the start of the COVID-19 pandemic in 2020.

LEARN MOREPRESS RELEASE

Survey: In 2024, CEOs Are Most Worried About a Recession & Inflation, But S…

January 10, 2024

PRESS RELEASE

As Labor Day Approaches, HR Leaders Say Hiring

August 29, 2023

IN THE NEWS

CEOs Are Predicting a Mild Recession in the U.S.

June 01, 2023

PRESS RELEASE

Global Productivity Growth Set to Disappoint Again in 2023

May 17, 2023

IN THE NEWS

Dana Peterson on Why Recession is Likely in 2023

April 20, 2023

PRESS RELEASE

Which Industries Will Start Shedding Jobs?

April 05, 2023